Today: Estimators

Goal: Explore generalization from samples to populations

Objectives: Show the biased or unbiased estimation via

- sample mean \(\bar{x}\)

- sample variance \(s^{2}\)

- sample standard deviation \(s\)

Demographics Example

From our Demographics Survey data of Math 32 students, suppose that the following is a sample of observations of heights (in inches):

\[\{x_{11} = 72, x_{12} = 61, x_{13} = 60, x_{14} = 75, x_{15} = 69\}\]

- then \(t_{1} = 67.4\) inches is the sample mean.

Suppose that the following is another sample of heights:

\[\{x_{21} = 66, x_{22} = 78, x_{23} = 78, x_{24} = 77, x_{25} = 64\}\]

- then \(t_{2} = 72.6\) inches is the sample mean.

Suppose that the following is another sample of heights:

\[\{x_{31} = 61, x_{32} = 59, x_{33} = 70, x_{34} = 61, x_{35} = 65\}\]

- then \(t_{3} = 63.2\) inches is the sample mean.

Observe: the sample mean (usually) changes upon a new set of observations

- Can we calculate the average height of UC Merced students?

- How can we calculate the average height of UC Merced students?

Thought: what if we take a mean of the sample means?

Estimators

Let \(T\) be a random variable and \(f\) be some calculation \[T = f(x_{1}, x_{2}, x_{3}, ...)\]

If we are trying to estimate a population parameter \(\theta\), we say that \(T\) is an unbiased estimator of \(\theta\) if \[\text{E}[T] = \theta\]

Today, we will look at situations where \(f\) is calculating the

- mean

- variance

- standard deviation

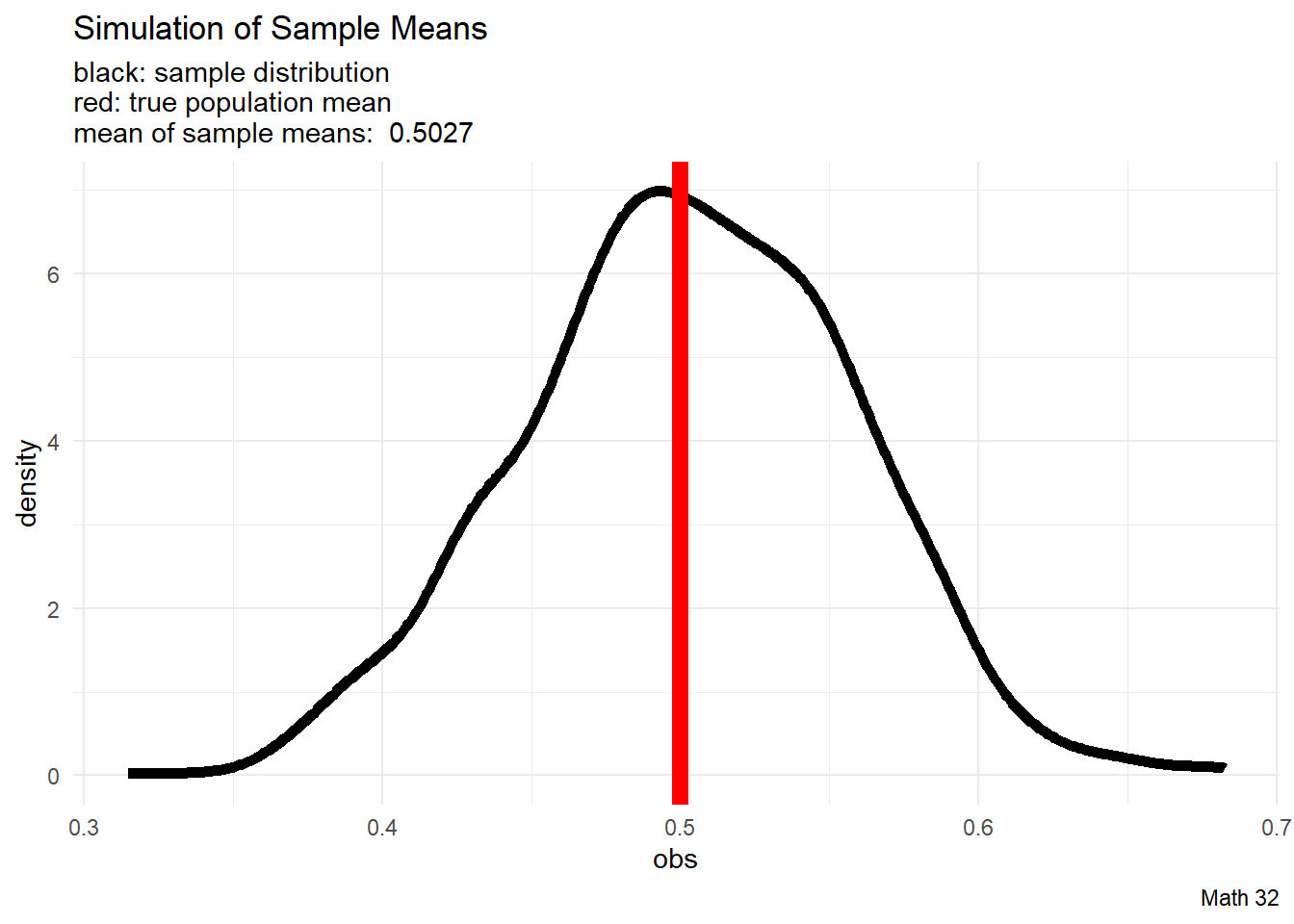

Mean

We will run simulations with \(X \sim U(0,1)\) because we know what the answers should be. The population mean is

\[\mu = \displaystyle\frac{a + b}{2} = \displaystyle\frac{1}{2}\]

N <- 1337 # number of iterations

n <- 25 # sample size

# pre-allocate vector of space for observations

obs <- rep(NA, N)

# run simulation

for(i in 1:N){

these_numbers <- runif(n, 0, 1) # sample n numbers from U(0,1)

obs[i] <- mean(these_numbers) #record average

}

# mean of observations

mean_of_obs <- mean(obs)

# make data frame

df <- data.frame(obs)

# visualization

df |>

ggplot(aes(x = obs)) +

geom_density(color = "black", size = 2) +

geom_vline(xintercept = 1/2, color = "red", size = 3) +

labs(title = "Simulation Sample Mean",

subtitle = paste("black: sample distribution\nred: true population mean\nmean of sample means: ", round(mean_of_obs, 4)),

caption = "Math 32") +

theme_minimal()Warning: Using `size` aesthetic for lines was deprecated in ggplot2 3.4.0.

ℹ Please use `linewidth` instead.

Loosely speaking, since the sampling distribution “lines up” with the population mean, we say that the sample median is an unbiased estimator of the population mean.

Therefore \(\text{E}[\bar{X}_{n}] = \mu\)

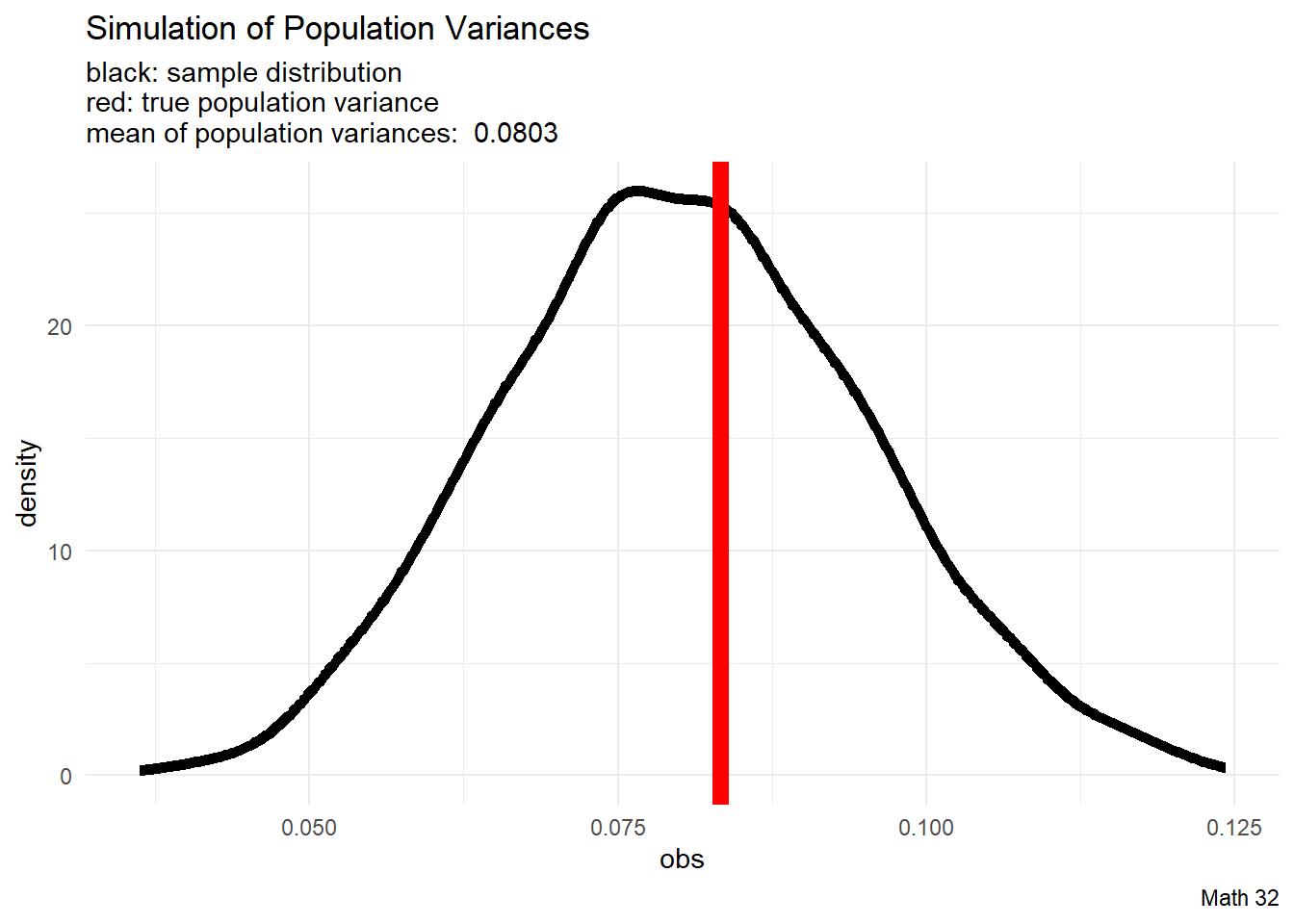

Population Variance

We will run simulations with \(X \sim U(0,1)\) because we know what the answers should be. The population variance is

\[\sigma^{2} = \displaystyle\frac{(b-a)^{2}}{12} = \displaystyle\frac{1}{12}\]

We will explore what happens if we apply the population variance formula

\[\sigma^{2} = \frac{1}{N}\displaystyle\sum_{i=1}^{N} (x_{i} - \mu)^{2}\]

to samples.

# user-defined function

pop_var <- function(x){

N <- length(!is.na(x)) #population size

mu <- mean(x, na.rm = TRUE) #population mean

# return population mean (note use of "N")

sum( (x - mu)^2 ) / N

}

N <- 1337 # number of iterations

n <- 25 # sample size

# pre-allocate vector of space for observations

obs <- rep(NA, N)

# run simulation

for(i in 1:N){

these_numbers <- runif(n, 0, 1) # sample n numbers from U(0,1)

obs[i] <- pop_var(these_numbers) #record population variance

}

# mean of observations

mean_of_obs <- mean(obs)

# make data frame

df <- data.frame(obs)

# visualization

df |>

ggplot(aes(x = obs)) +

geom_density(color = "black", size = 2) +

geom_vline(xintercept = 1/12, color = "red", size = 3) +

labs(title = "Simulation of Population Variances",

subtitle = paste("black: sample distribution\nred: true population variance\nmean of population variances: ", round(mean_of_obs, 4)),

caption = "Math 32") +

theme_minimal()

Loosely speaking, since the sampling distribution tends to underestimate the population variance, we say that the population variance (with \(N\)) is a biased estimator of the population variance.

Bessel’s Correction

Can we rescale the process for computing variance so that the operation is an unbiased estimator for the population variance?

Let \(X_{i}\) be a set of \(n\) i.i.d. random variables from the same distribution with the same population variance \(\sigma^{2}\). By independence, there is zero covariance.

We will compute the value of \(k\) so that

\[\text{E}\left[k \cdot \frac{\sum_{i=1}^{n}(X_{i} - \bar{X}_{n})^{2}}{n}\right] = \sigma^{2}\]

Lemma: \(\text{Var}(X_{i} - \bar{X}_{n}) = \displaystyle\frac{n-1}{n} \cdot \sigma^{2}\)

We have derived the formula for the sample variance

\[S_{n}^{2} = \displaystyle\frac{1}{n-1}\displaystyle\sum_{i=1}^{n}(X_{i} - \bar{X}_{n})^{2}\]

That is, the “\(n-1\)” (Bessel’s correction) is in place so that the sample variance \(s^{2}\) is an unbiased estimator of the population variance \(\sigma^{2}\)

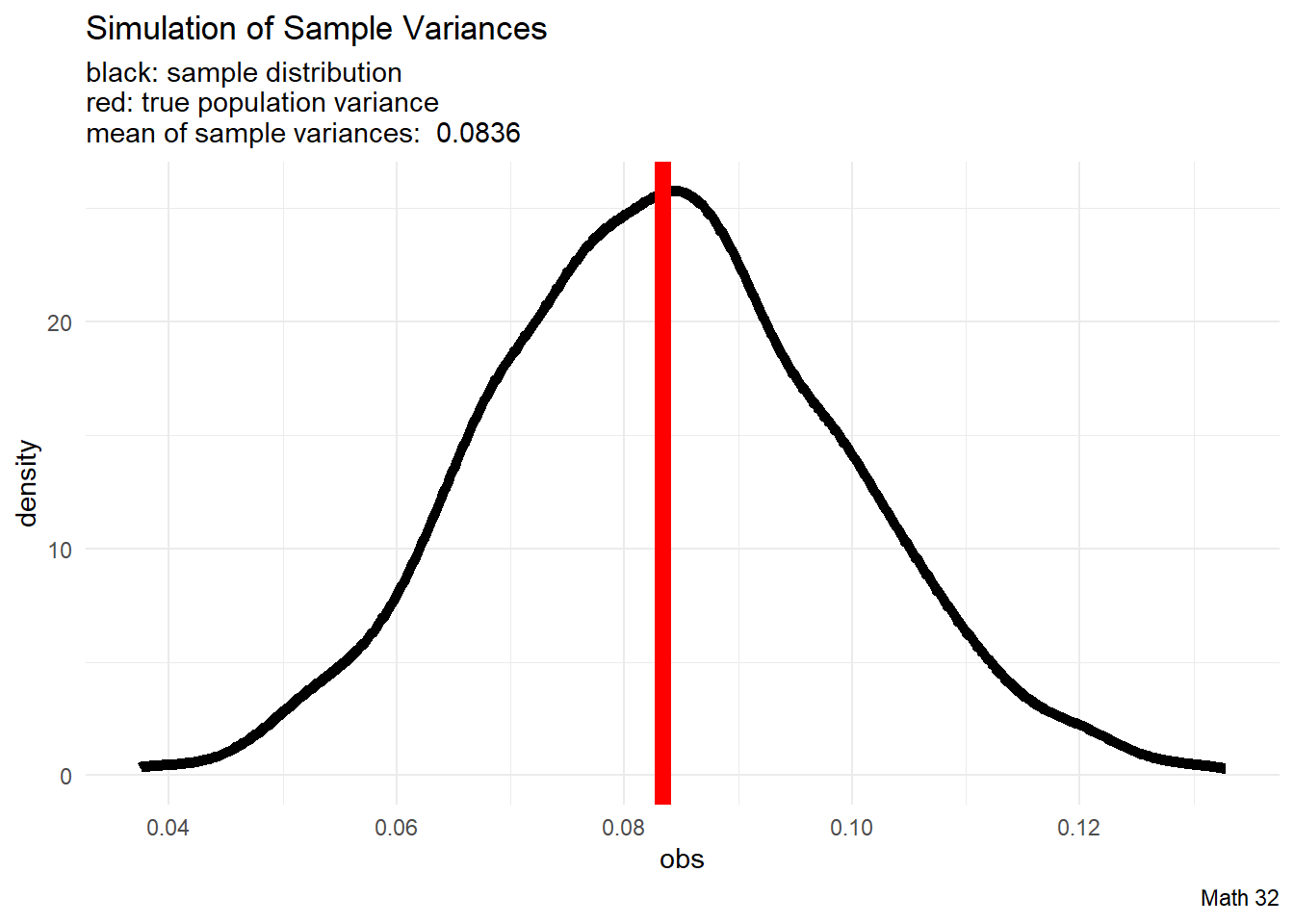

Sample Variance

We will run simulations with \(X \sim U(0,1)\) because we know what the answers should be. The population variance is

\[\sigma^{2} = \displaystyle\frac{(b-a)^{2}}{12} = \displaystyle\frac{1}{12}\]

We will explore what happens if we apply the sample variance formula

\[s^{2} = \frac{1}{n-1}\displaystyle\sum_{i=1}^{n} (x_{i} - \mu)^{2}\]

to samples.

# user-defined function

samp_var <- function(x){

n <- length(!is.na(x)) #sample size

xbar <- mean(x, na.rm = TRUE) #sample mean

# return population mean (note use of "n-1")

sum( (x - xbar)^2 ) / (n-1)

}

N <- 1337 # number of iterations

n <- 25 # sample size

# pre-allocate vector of space for observations

obs <- rep(NA, N)

# run simulation

for(i in 1:N){

these_numbers <- runif(n, 0, 1) # sample n numbers from U(0,1)

obs[i] <- samp_var(these_numbers) #record sample variance

}

# mean of observations

mean_of_obs <- mean(obs)

# make data frame

df <- data.frame(obs)

# visualization

df |>

ggplot(aes(x = obs)) +

geom_density(color = "black", size = 2) +

geom_vline(xintercept = 1/12, color = "red", size = 3) +

labs(title = "Simulation of Sample Variances",

subtitle = paste("black: sample distribution\nred: true population variance\nmean of sample variances: ", round(mean_of_obs, 4)),

caption = "Math 32") +

theme_minimal()

Loosely speaking, since the sampling distribution “lines up” with the population variance, we say that the sample variance (with \(n-1\)) is an unbiased estimator of the population variance.

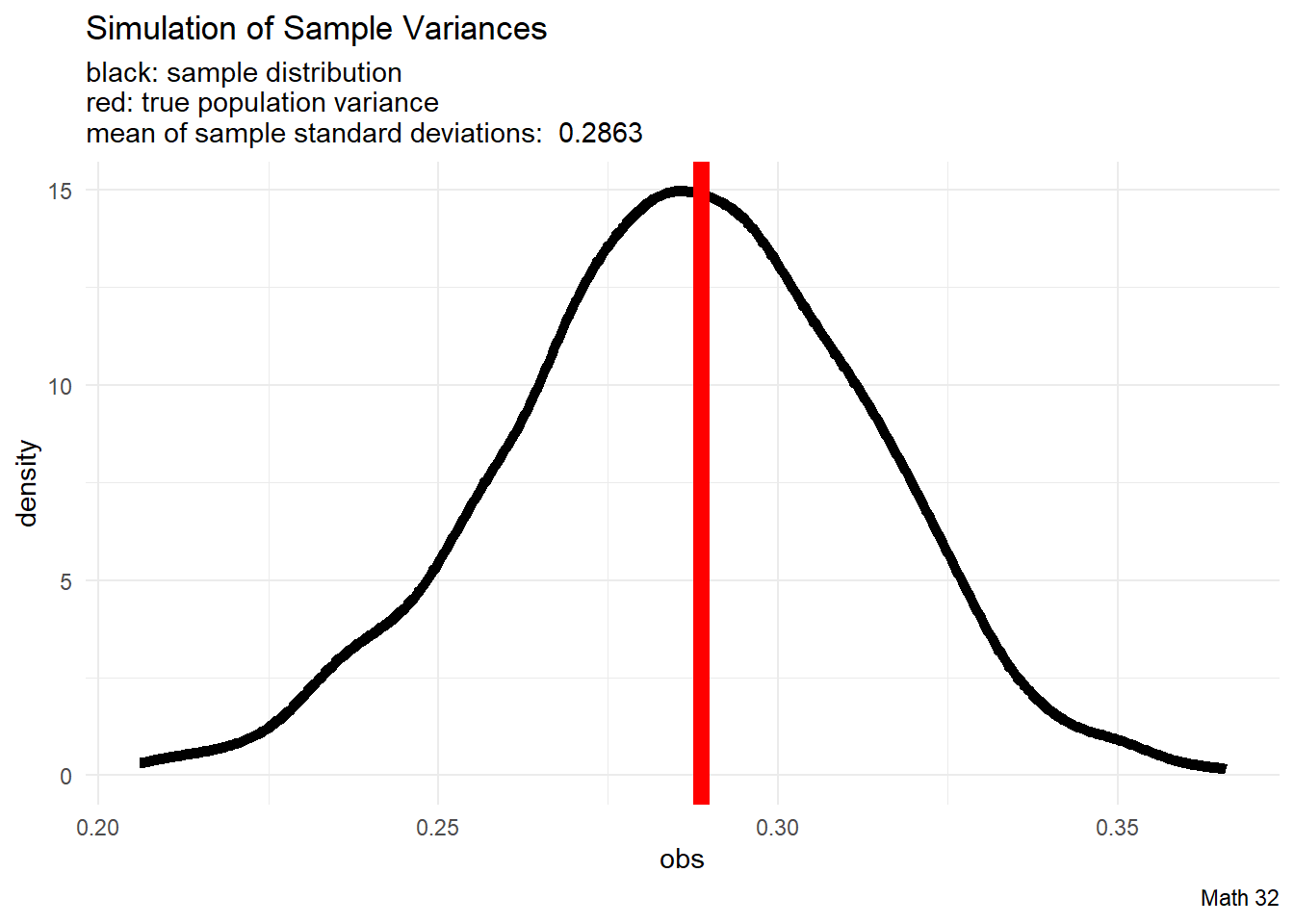

Sample Standard Deviation

We will run simulations with \(X \sim U(0,1)\) because we know what the answers should be. The population standard deviation is

\[\sigma = \sqrt{\displaystyle\frac{(b-a)^{2}}{12}} = \sqrt{\displaystyle\frac{1}{12}}\]

We will explore what happens if we apply the sample variance formula

\[s = \sqrt{\frac{1}{n-1}\displaystyle\sum_{i=1}^{n} (x_{i} - \mu)^{2}}\]

to samples.

# user-defined function

samp_var <- function(x){

n <- length(!is.na(x)) #sample size

xbar <- mean(x, na.rm = TRUE) #sample mean

# return population mean (note use of "n-1")

sum( (x - xbar)^2 ) / (n-1)

}

N <- 1337 # number of iterations

n <- 25 # sample size

# pre-allocate vector of space for observations

obs <- rep(NA, N)

# run simulation

for(i in 1:N){

these_numbers <- runif(n, 0, 1) # sample n numbers from U(0,1)

obs[i] <- sqrt(samp_var(these_numbers)) #record sample standard deviation

}

# mean of observations

mean_of_obs <- mean(obs)

# make data frame

df <- data.frame(obs)

# visualization

df |>

ggplot(aes(x = obs)) +

geom_density(color = "black", size = 2) +

geom_vline(xintercept = sqrt(1/12), color = "red", size = 3) +

labs(title = "Simulation of Sample Variances",

subtitle = paste("black: sample distribution\nred: true population variance\nmean of sample standard deviations: ", round(mean_of_obs, 4)),

caption = "Math 32") +

theme_minimal()

Let \(X_{i}\) be a set of \(n\) i.i.d. random variables from the same distribution with the same population standard deviation \(\sigma\). To avoid trivial situations, assume non-zero variance, so \(\sigma \neq 0\).

If \(s = \sqrt{ \displaystyle\frac{\sum_{i=1}^{n}(X_{i} - \bar{X}_{n})^{2}}{n-1} }\) was an unbiased estimator, then \(\text{E}[s] = \sigma\)

However, by Jensen’s Inequality, since \(g(x) = x^{2}\) is a convex function,

\[\sigma^{2} = \text{E}[S_{n}^{2}] > \left(\text{E}[S_{n}]\right)^{2}\]

and it follows that \(\text{E}[S_{n}] < \sigma\). Due to the underestimation, sample standard deviation \(s\) is a biased estimator of population standard deviation \(\sigma\).

\[~\]

However, in practice, the discrepancy is usually so small that it is ignored.

Looking Ahead

due Fri., Mar. 24:

- LHW8

no lecture on Mar. 24, Apr. 3

Exam 2 will be on Mon., Apr. 10